Offsetting Liquidation Engine Profits with Market Maker Losses

A Market Maker Proposal

For the Digitex Futures exchange to ensure liquidity and tight bid/ask spreads without trading against the interests of its traders, we have always maintained that our automated market makers (which represent 10% of the supply of DGTX) will break even and will not make profits. However, in this second proposal, we put forward an alternative, more effective way for the market makers to function. They would help maintain a large insurance fund and create liquid futures markets, offsetting Liquidation Engine profits by making losses. Let’s take a look at the details.

Market Maker Losses: Proposal Number 2

Maintain Large Insurance Fund And Create Liquid Futures Markets By Offsetting Liquidation Engine Profits With Market Maker Losses

By combining the Liquidation Engine, automated Market Makers and the Insurance Fund, the exchange would be able to guarantee its liabilities whilst also creating liquid futures markets with tight bid/ask spreads.

Profits made by the Liquidation Engine are given back to the market in the form of losses made by the exchange’s very active automated Market Makers. This will attract large numbers of traders who will compete for their share of those losses, further increasing liquidity.

Market Maker Proposal Key Points

- The Digitex Futures exchange will open its doors with an Insurance Fund/Market Maker balance of 100 million DGTX tokens (10% of the total supply of DGTX) that was set aside in the ICO for the purpose of market making.

- The Liquidation Engine is essentially a profit-making mechanism that adds funds to this Insurance Fund. The Liquidation Engine effectively penalizes highly leveraged traders who put the exchange at risk by allowing their account balances to drop below the required level to maintain their open position.

- The automated Market Makers would, therefore, be a loss-making mechanism that purposely loses the profits made by the Liquidation Engine by constantly placing bids and offers with very tight spreads, even in volatile market conditions, creating liquid futures markets in the process.

- The operational parameters of the automated Market Makers are constantly adjusted to keep their losses in line with the profits made by the Liquidation Engine, thus permanently maintaining the Insurance Fund balance at 100m DGTX.

- Active market making by the exchange without any need or incentive to make a profit from its users from this activity creates liquid futures markets without having to give preferential treatment and unfair advantages to third-party market makers.

- Allowing the automated Market Makers to lose money means they can be much more active and can keep bid/ask spreads much tighter, especially in volatile markets, than if they had to break even.

- Being able to operate automated Market Makers that lose money removes any conflict of interest that would arise if the exchange was trading profitably against its own users.

- Losses made by the exchange’s automated Market Makers will attract large numbers of traders who will compete for their share of those losses, further increasing liquidity.

- Profits made by the Liquidation Engine are not a conflict of interest because traders can avoid contact with the Liquidation Engine if they so wish by managing their positions more responsibly.

- The profits made by the Liquidation Engine typically come from high risk, highly leveraged traders who accept that forcing the exchange to take over their position may result in bigger losses than if they managed their position more responsibly by not allowing their account balance to drop below the required amount. Therefore, it is very possible for traders to avoid any contact with the Liquidation Engine if they wish.

- Just as traders can avoid contact with the Liquidation Engine, they can also increase their chances of profiting from the automated Market Maker losses through a disciplined scalping style trading strategy that specifically targets the Market Makers.

- This system effectively takes DGTX tokens from high risk, highly leveraged traders who are gambling on price movements of the underlying instruments and transfers them to the more methodical short term traders whose strategy is specifically tailored toward trading against the automated Market Makers.

- Loss-making automated Market Makers give disciplined, short term traders a mechanical edge that is constantly working in their favor.

- Competition amongst traders for their share of the automated Market Makers losses will encourage active trading styles, creating very liquid futures markets.

- This mechanical edge in the traders’ favor will create more winning traders than traditional exchanges.

- A zero-fee futures market that also has a mechanical edge built into the trader’s favor is the polar opposite of the traditional futures market whose trading fees and preferential treatment to third-party market makers make it almost impossible for retail traders to make a profit.

- The increased chances of becoming a winning trader will make viral marketing campaigns and ‘refer a friend’ features built into the platform highly effective at attracting large numbers of new traders, further increasing liquidity.

- As a reminder, large numbers of new traders who are attracted to the exchange to compete for their share of the Market Maker losses must all first buy DGTX tokens to do so.

If you have questions about the points laid out in this proposal, be sure to catch Adam’s AMA live from Moscow today at 5 pm CET (11 am EST). In this Q&A session, Adam will answer your questions about the Liquidation Engine and Insurance Fund (Addendum II) and also discuss the details of the above proposal for market maker losses. Don’t miss it!

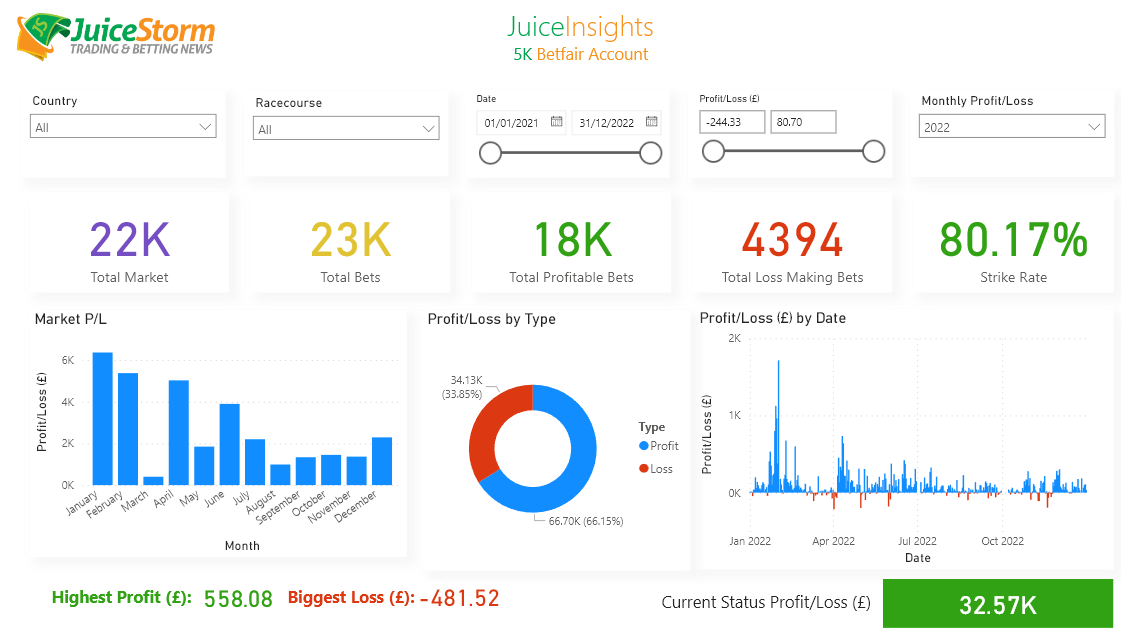

In 2021 TradeHost traded 7,937 Betfair UK, IE, US & AU horse racing and greyhound markets.

2022 saw TradeHost become even more profitable with 22,698 Betfair markets traded.

2023 less markets were traded – 17,459 – but a with a similar profit to 2022.

All trades and bets were streamed live on JuiceStorm TV which was was watched by 124,209 traders in 2022.

All results for the 48,094 Betfair markets traded are here and the charts are here.

Top 100 Comments on JuiceStorm.com

Successful Betfair Traders have the simplest Betfair Trading systems. The difference is their selection process, experience and execution level. Get that difference for yourself with automated trading by TradeHost.